Executive Summary

Africa’s grain industry is large and growing, but marked by a widening gap between rising demand and domestic supply. Total cereal consumption on the continent reached about 283 million metric tons in 2024, and is forecast to climb to 311 million tons by 2035, reflecting a steady growth of ~0.9% per year. However, production growth has lagged behind population-driven demand. Africa’s farms produced roughly 216–218 million tons of cereals in 2023-2024, leaving a deficit filled by imports of around 70+ million tons annually. The market value of Africa’s grain consumption was estimated at $126.1 billion in 2024, expected to rise to $150.5 billion by 2035. Maize is the dominant grain produced, while wheat and rice are heavily imported to meet consumer needs. Key drivers of growth include rapid population expansion, urbanization, and dietary shifts, alongside government initiatives for food security. At the same time, significant challenges – from low farm productivity and climate risks to infrastructure and policy constraints – hinder the continent’s ability to achieve self-sufficiency. Major grain producers like Nigeria, Ethiopia, and Egypt lead output, yet countries such as Egypt, Algeria, and Morocco are among the world’s largest grain importers. Strategic opportunities exist to invest in improved technologies, irrigation, and value chains, which could unlock Africa’s vast agricultural potential (the continent holds 60–65% of the world’s uncultivated arable land) and substantially boost grain output. In summary, Africa’s grain market is poised for moderate growth, with future outlook hinging on addressing structural challenges – success could transform Africa from a heavy grain importer toward greater self-reliance, while failure to act risks a doubling of the import bill in the next decade. The following report provides an in-depth analysis of the African grain industry, covering market size, segments, regional dynamics, trade flows, production/consumption trends, drivers and challenges, policy landscape, competitive players, technological innovations, and investment opportunities for the period through 2035.

Market Overview

Grains (cereals) are the staple backbone of Africa’s food security and agricultural economy. They account for a large share of daily caloric intake for hundreds of millions of Africans, especially in the form of maize meal, wheat flour, rice, sorghum, and millet-based foods. The grain sector’s importance is underscored by chronic supply-demand imbalances: Africa remains a net importer of cereals, reflecting the continent’s difficulty in meeting demand through domestic production. In 2021, African countries spent over $100 billion on food imports, resulting in a net import bill of about $39 billion – much of this on basic staples like wheat, maize, and rice. This dependency has persisted even though agriculture is a livelihood for the majority of Africans and contributes around 15% of continental GDP. Rapid population growth (Africa’s population is rising ~2.7% per year and is projected to reach ~2 billion by 2050) is driving up grain consumption, but production has struggled to keep pace due to low yields and other constraints. As a result, Africa currently produces only roughly 7–8% of global grain output while accounting for about 17% of the world’s population, indicating a significant grain deficit. The imbalance is especially acute for wheat and rice, which have seen soaring demand in African urban areas but limited domestic cultivation. Regional disparities also characterize the market: North African nations (e.g. Egypt, Algeria, Morocco) have relatively high yields in irrigated wheat and rice farming but still face deficits, whereas many Sub-Saharan African countries rely on rain-fed production of maize, sorghum, and millet with highly variable outputs. Overall, the African grain industry today is one of high strategic importance and unrealized potential – it is critical for food supply and price stability, yet remains vulnerable to climatic shocks and global market volatility. This report will detail the current market structure and highlight the trends shaping Africa’s grain sector.

Market Size and Growth (Historical and Forecast to 2035)

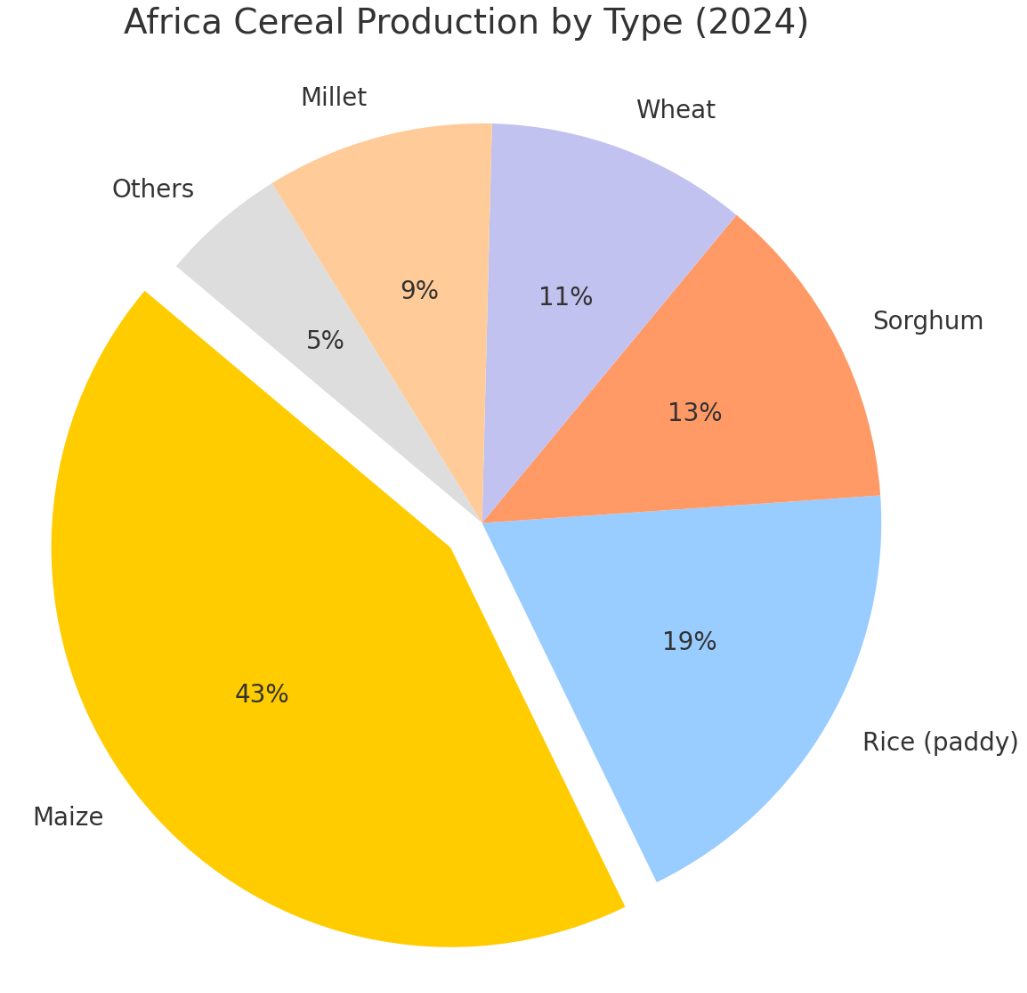

Overall Market Size: The total cereal consumption in Africa (including maize, wheat, rice, sorghum, millet, barley, and other grains) has grown steadily over the past decade. In 2013, Africa’s cereal use was approximately 230 million tons; by 2024 it reached 283 million tons, reflecting an average annual growth of ~1.9%indexbox.io. This growth has been largely demand-driven, fueled by population increases and changing diets. Figure 1 illustrates the composition of Africa’s cereal production by grain type in 2024 – maize alone accounts for about 43% of output, reflecting its central role.

xxx

Figure 1: Share of Africa’s cereal production by grain type in 2024. Maize dominates at 43% of total output, followed by rice (paddy) at ~19% and sorghum at 13%. Wheat and millet each contribute roughly 9–11%, with other minor cereals (e.g. barley, fonio, oats) making up the remainder. These shares underscore maize’s primacy in African agriculture, while highlighting that wheat (despite high consumption) constitutes a relatively small portion of domestic production.

In value terms, Africa’s grain market was worth about $126 billion in 2024, up from ~$110 billion a decade earlier. Market value has risen both due to volume increases and generally higher grain prices in recent years. Looking ahead, the forecast to 2035 indicates continued moderate growth. Africa’s cereal consumption is projected to reach 311 million tons by 2035, up from 283 million in 2024. This represents a CAGR of ~0.9% in volume from 2024 to 2035 – a slower growth rate than the previous decade, reflecting expectations of some demand deceleration. In monetary terms, the market value is expected to grow at ~1.6% annually, reaching an estimated $150.5 billion by 2035 (in nominal wholesale prices). The slight difference between volume and value growth rates is attributable to anticipated price increases and a shift toward higher-value grains and processed products.

Historical Growth: The historical trend (2010s into early 2020s) showed relatively stable growth in grain consumption with minor year-to-year fluctuations. For instance, consumption dipped slightly during 2019–2020 (due to factors like COVID-19 disruptions and high prices) but rebounded by 2023–2024. Production has increased more slowly, constrained by yield plateaus and limited land expansion. As a result, import volumes expanded – cereal imports grew at ~2.3% per year from 2013 to 2024. By 2024, Africa was importing roughly 71 million tons of cereals (a 15% jump from the previous year as countries restocked and demand recovered). This import dependency has become a structural feature of the market size.

Per Capita Perspective: With population growth outpacing grain output, per capita grain availability has been nearly flat or declining in some regions. Africa’s population growth (~3% annually in many countries) exceeds the growth in cereal production (~1–2%), implying a widening food gap. Without significant productivity improvements, the continent’s reliance on imports to meet per capita needs will persist. The forecast to 2035 assumes no drastic breakthrough in yields – if that holds, the grain import bill could swell further (potentially 50–100% higher by the mid-2030s).

In summary, Africa’s grain market is large and expanding, but growth is primarily on the consumption side. By 2035, demand will comfortably exceed 300 million tons annually, yet the key uncertainty is how much of that demand can be met by African producers. The stakes are high: closing the growth gap via investment and reforms could turn the grain sector into a growth engine, whereas business-as-usual will see Africa’s grain import dependence deepen over the next decade.

Key Segments by Grain Type

Africa’s grain production and consumption can be segmented by crop type, with maize, wheat, rice, sorghum, and millet being the most important cereals (alongside smaller amounts of barley, oats, teff, and others). Each grain plays a distinct role in the African diet and agricultural system:

- Maize (Corn): Maize is the leading cereal in Africa by area and output. In 2024 African farmers produced about 94 million metric tons of maize, accounting for roughly 43% of all cereal production on the continent. Maize is a staple food for most of Sub-Saharan Africa – it is consumed as porridge, meal (ugali, nshima, sadza), bread (maize flour), and snacks, and also serves as a key ingredient in animal feed. Africa consumes about 109 million tons of maize per year (2024), slightly more than it produces, with some imports to meet the deficit. The region is predominantly a white maize market (for human consumption), unlike the Americas which focus on yellow maize for feed. Major producers include South Africa (the continent’s largest maize producer), Nigeria, Ethiopia, Tanzania, and Malawi. South Africa alone often produces 15–17 Mt/year and is a net exporter of maize, while Nigeria (~12 Mt) and Ethiopia (10 Mt) consume most of their output domestically. Thanks to government support and improved seeds, African maize production has been rising (+2.5% per year), though yields (averaging ~2 tons/ha) remain well below global averages. Maize trade: Southern Africa sometimes has surplus (South Africa, Zambia) that is exported within Africa or to international markets, whereas countries like Kenya, Zimbabwe, and Egypt import maize in years of shortfall. Overall, maize in Africa is relatively self-sufficient – imports constituted only ~19 Mt in 2024 (about 27% of Africa’s total cereal imports, and under 15% of its maize consumption). Continued investments in hybrid maize varieties, fertilizer use, and irrigation could further boost Africa’s maize output, making it a potential export crop for the region.

- Wheat: Wheat is Africa’s second-most consumed cereal but is mostly imported due to limited suitable growing areas. Annual wheat consumption in Africa reached ~73 million tons in 2024, driven by urbanization and the popularity of wheat-based foods (bread, pasta, couscous, pastries). However, Africa’s wheat production is only ~20–25 million tons per year, covering barely one-third of its needs. The continent’s major wheat-growing zones are in North Africa (Morocco, Egypt, Algeria, Tunisia) and parts of East Africa (Ethiopia, Sudan, Kenya) and Southern Africa (South Africa, Zimbabwe). Egypt is the top producer (~9–10 Mt in a good year) followed by Ethiopia (~5 Mt) and Morocco (which varies between 3–7 Mt depending on rainfall). Despite these outputs, countries like Egypt, Algeria, Nigeria, and Sudan have huge demand that far outstrips local production, necessitating imports. In 2024, Africa imported an estimated 47 million tons of wheat, making wheat by far the largest imported grain (about 67% of total cereal imports by volume). This heavy reliance has made Africa vulnerable to global market disruptions – for example, 37% of Sub-Saharan Africa’s wheat and maize imports came from Russia and Ukraine prior to 2022, so the war in Ukraine raised serious food security concerns. Wheat imports primarily come from the Black Sea region (Russia, Ukraine), the European Union, Canada, the United States, and Australia. Given the high import bill, many governments have set goals for wheat self-sufficiency. Ethiopia, for instance, has rapidly expanded irrigated wheat cultivation and in 2023 claimed to be nearing self-sufficiency, potentially eliminating the need for $600 million in annual imports. Nigeria and Sudan are promoting heat-tolerant wheat varieties to boost output. Still, wheat faces agronomic challenges in Africa (it prefers temperate climates or cool seasons), so closing the gap will be difficult. Wheat remains indispensable for North African diets (e.g. Egypt’s per capita wheat consumption is among the highest in the world, with the government subsidizing bread for millions) and is increasingly important across Africa’s cities. Unless production dramatically improves, Africa’s wheat imports are expected to stay high, making it the most strategic grain in terms of trade and food policy.

- Rice: Rice has emerged as a staple across Africa, especially in West Africa and urban centers, with demand rising faster than any other cereal. Africa produced about 41 million tons of paddy rice in 2024, equivalent to roughly ~27 million tons of milled rice. Major rice-growing countries include Nigeria (the largest producer in Africa, ~9 Mt paddy), Egypt (~6 Mt paddy under irrigation in the Nile Delta), Madagascar, Tanzania, Mali, Guinea, and Côte d’Ivoire. Despite production growth (+3.1% per year on average) thanks to initiatives like New Rice for Africa (NERICA) varieties and expanded irrigation in some areas, consumption still far exceeds domestic output. Rice is the most consumed cereal in several West African countries and is favored in urban diets for its convenience. Over the last 15 years, rice consumption in Sub-Saharan Africa nearly doubled, propelled by population growth, urbanization, and dietary shifts toward rice. This surge in demand has made Sub-Saharan Africa the world’s largest rice-importing region as of 2025, surpassing even Southeast Asia. In 2024, Sub-Saharan Africa’s rice imports hit a record, forecast around 28–30 million tons (milled), which is a majority of the region’s ~36 Mt total rice consumption. Key importers include Nigeria, Côte d’Ivoire, Senegal, Ghana, and South Africa, with rice imports mostly sourced from Asian exporters – India (the leading supplier), Thailand, Vietnam, Pakistan, and others. India’s policy decisions (such as export bans or taxes on rice) have an outsized impact on African markets; for example, India’s export restrictions in 2023 prompted African buyers to seek alternative suppliers like Thailand and Pakistan, until India lifted most restrictions in late 2024 leading to a rebound in exports to Africa. Given rice’s importance, many African nations have launched programs to boost local rice production – e.g. Nigeria’s central bank funding for rice farmers and millers, Mali’s expansion of irrigation (Office du Niger) for rice, and Ethiopia’s introduction of rice in suitable lowland areas. These efforts have had mixed success. Import dependency for rice remains around 40–50%, and African consumers are highly exposed to global rice price swings. Nonetheless, the long-term goal in many countries is to achieve self-sufficiency in rice, which if attained could significantly reduce Africa’s food import bill.

- Sorghum and Millet: Sorghum and millet are traditional cereals vital for food security in arid and semi-arid regions of Africa. They are drought-tolerant, hardy grains predominantly grown by smallholder farmers for subsistence, and are especially important in the Sahel, Horn of Africa, and parts of Southern Africa. In 2024, Africa’s sorghum production was about 28 million tons, making Africa the largest sorghum-producing continent (accounting for the bulk of global sorghum used for human food). Millet (including pearl millet and finger millet) output is slightly less – estimates range from 15 to 20 million tons per year in Africa (exact figures vary, but West Africa grows the lion’s share of the world’s millet). Leading producers of sorghum are Nigeria (often the world’s #2 producer after the US, with ~6–7 Mt), Sudan (~5 Mt), Ethiopia (~5 Mt), Niger, and Mali. For millet, Niger is a top producer (~3–5 Mt), along with Nigeria, Mali, Burkina Faso, and Chad. These crops are staples for millions – made into foods like tuwo (millet porridge) in West Africa, injera (teff-sorghum bread) in Ethiopia (sorghum often substitutes for teff), and ugali in parts of East Africa. Virtually all sorghum and millet produced in Africa is consumed locally, as these grains seldom enter major international trade. They collectively comprised roughly 21% of Africa’s cereal consumption in recent years. Imports of sorghum/millet are minimal (occasionally a few hundred thousand tons moved as food aid or regional trade). Both crops have seen relatively slow production growth (~0.8% per year for sorghum), as they are often grown in marginal conditions with low inputs. However, improved varieties and agronomic practices are being introduced (e.g. improved millet cultivars through ICRISAT, and sorghum hybrids in Sudan) to raise yields. Sorghum also has a commercial use in brewing – some African breweries use sorghum or millet as a malt substitute in beer, providing a market for farmers. Overall, while not as “visible” as maize, wheat, or rice in the urban market, sorghum and millet remain crucial for food security in dryland rural Africa and will continue to be important segments of the grain sector, particularly under climate change pressures that make these hardy crops even more valuable.

- Other Grains (Barley, Teff, Others): Several other cereals play niche roles. Barley is grown in the highlands of North Africa and Ethiopia (~3–4 million tons/year in Africa) mainly for beer brewing and some food use (e.g. in soups/porridge). Morocco and Ethiopia are leading barley producers. Barley imports (~3.7 Mt in 2024) supply big North African breweries and feedlots (e.g. for horse and camel feed in Morocco) – imported barley comes from France, Ukraine, Russia, etc. Teff, a cereal unique to Ethiopia/Eritrea, is central to Ethiopian diets (used for injera flatbread); Ethiopia produces ~5 Mt of teff annually, which doesn’t show up in many international statistics but is about 17% of Ethiopia’s cereal output. Fonio, African rice (Oryza glaberrima), triticale, oats, and quinoa are among other grains produced in small quantities. Cumulatively, these “other cereals” are a tiny fraction (<5%) of Africa’s grain volume. Some, like fonio (a nutritious but low-yield grain in West Africa) and quinoa (being trialed in dry parts of Kenya, etc.), have niche markets and development interest. Overall, maize, wheat, rice, sorghum, and millet together constitute the vast majority of Africa’s grain industry (over 95% of production and consumption), and our analysis will primarily focus on these key segments.

Regional and Country Analysis

The African grain landscape varies widely by region and country, with distinct top producers, consumers, and importers. Here we examine the regional profiles and highlight key countries:

Top Producing Regions & Countries: Grain production is concentrated in a few populous countries with favorable agro-climates. In 2024, three countries – Ethiopia, Nigeria, and Egypt – accounted for ~38% of Africa’s total cereal output:

- Ethiopia: ~30 Mt (primarily maize, sorghum, teff, and wheat). Ethiopia’s highlands are productive for cereals; it leads in sorghum and teff and is among top maize and wheat producers.

- Nigeria: ~29 Mt (maize, sorghum, millet, rice). Nigeria has Africa’s largest population and a correspondingly large cereal output across several crops (it is the #1 producer of maize, cassava, yams, and sorghum in Africa). However, Nigerian yields are generally low, and it also has high consumption needs.

- Egypt: ~23 Mt (wheat, maize, rice). Egypt’s intensive irrigated agriculture in the Nile Valley and Delta makes it Africa’s top wheat and rice producer and a significant maize producer, all on relatively small land area with high yields.

The next tier of producers includes:

- South Africa (~17–18 Mt, mostly maize and some wheat/barley). South Africa’s commercial farms make it the only African country regularly exporting surplus grain (maize) outside the continent.

- Tanzania (~10 Mt, maize and rice dominate). Tanzania’s varied climate allows production of maize in the highlands and rice in river basins.

- Mali (~9 Mt, millet, sorghum, rice). Mali is a major Sahelian producer with large millet/sorghum output and an expanding irrigated rice sector.

- Sudan (~7–8 Mt, sorghum and millet). Sudan’s Gezira Scheme historically was a big sorghum producer; rain-fed farms also contribute.

- Ethiopia’s neighbors like Sudan, Kenya, Uganda, and West African nations like Ghana, Niger, Burkina Faso, Côte d’Ivoire, and Ghana each produce on the order of 3–6 Mt of various grains. For instance, Niger (mostly millet, ~4 Mt) and Guinea (rice, ~3–4 Mt) were notable contributors. These and other countries collectively form the remaining one-third of output.

In regional terms:

- West Africa (especially the Sahel and savanna zones) grows much of Africa’s millet, sorghum, and rain-fed rice, with Nigeria, Niger, Mali, Burkina Faso being key contributors.

- East Africa (Ethiopia, Kenya, Tanzania, Uganda) is a major maize and sorghum zone, plus teff (Ethiopia) and rice (Tanzania).

- Southern Africa (South Africa, Zambia, Malawi, Zimbabwe) focuses on maize; South Africa and Zimbabwe also grow some wheat and barley.

- North Africa (Egypt, Morocco, Algeria, Tunisia) leads in wheat and barley under rain-fed and irrigated systems, and also rice in Egypt. North African countries often have the highest yields (thanks to irrigation and mechanization) but are constrained by limited arable land and water.

Top Consuming Countries: Not surprisingly, the largest consumers of grain overlap with the largest producers, adjusted for imports. In 2024, the three largest grain consumers in Africa were Egypt (38 Mt), Ethiopia (31 Mt), and Nigeria (29 Mt), which together accounted for about 35% of Africa’s total consumption:

- Egypt – 38 Mt: Egypt’s huge wheat consumption (for bread) plus significant maize (for food and feed) and rice intake make it the #1 consumer. Egypt’s consumption is buoyed by a population of ~105 million and diets centered on wheat bread (partly subsidized by the government) and rice.

- Ethiopia – 31 Mt: Ethiopians consume large amounts of grain per capita, including teff, maize, sorghum, and wheat for injera and porridges. Rapid population growth (~120 million people) has pushed Ethiopia’s grain consumption high.

- Nigeria – 29 Mt: Nigeria, with over 200 million people, has a diverse cereal consumption (maize for traditional dishes, rice which is extremely popular, sorghum for porridge/beer, and growing wheat-based products demand). Despite high production, Nigeria still must import wheat and rice to satisfy its 29 Mt consumption.

Other notable consuming nations (with their 2024 consumption) include:

- South Africa (~16–18 Mt): Maize is a staple (both for food and as animal feed in an advanced livestock sector) and wheat consumption is also high (mostly imported) along with some rice.

- Algeria (~10–11 Mt): Almost entirely wheat (for bread and couscous) – Algeria is one of the world’s top per-capita wheat consumers – plus some barley for couscous/feed.

- Morocco (~9–10 Mt): Mostly wheat and barley for food; also significant corn imports for feed.

- Tanzania (~9 Mt): Maize is the mainstay, along with rice in the diet.

- Kenya (~6–7 Mt): Dominated by maize (the staple ugali), but also wheat (bread, chapati) which is largely imported.

- Sudan (~6 Mt): Sorghum is the staple (for asida porridge and kisra bread), plus wheat (urban bread consumption).

- Mali (~5–6 Mt): Millet, sorghum, and rice are major foods.

In general, North African countries have the highest per-capita grain consumption (mostly wheat), and West African coastal countries have high rice consumption. Eastern and Southern Africa rely heavily on maize per capita.

Top Importers: Africa’s grain import needs are concentrated in certain countries, mostly those with large populations and limited arable land. The five largest cereal importing countries in Africa (by volume) are:

Figure 2: Top African cereal importers in 2024, in million metric tonsEgypt, Algeria, and Morocco together accounted for over half of all African grain imports.

As shown in Figure 2, the biggest importers are:

- Egypt – about 15 Mt of cereal imports in 2024. (Primarily wheat >10 Mt, as well as maize for livestock feed. Egypt’s heavy imports reflect its large food subsidy program and limited land for wheat cultivation beyond what is already irrigated.)

- Algeria – 13 Mt. (Almost entirely wheat; Algeria imports ~8–9 Mt of wheat annually, among the top three global wheat importers, plus some maize and barley for feed.)

- Morocco – 11 Mt. (Mix of wheat and maize. In drought years Morocco’s grain imports surge due to poor domestic harvests; 2024 saw high imports after dry conditions.)

- Tunisia – 5 Mt. (Mostly wheat; Tunisia typically imports 2 Mt of wheat, plus barley and corn each ~1 Mt.)

- Kenya – ~3.9 Mt (5.5% of Africa’s imports). (Kenya imports maize from regional neighbors in drought years and ~2 Mt of wheat annually from global markets, since local wheat production is small. Rice is also imported ~0.6 Mt.)

Other significant importers include South Africa (~3.3 Mt net imports in 2024, largely wheat as it imports 50% of its wheat needs while exporting maize), Senegal (~1.4 Mt, mostly rice and wheat), Libya (~1.4 Mt, reliant on wheat imports), Angola (~1.2 Mt, mainly rice and wheat), Nigeria (though a major producer, Nigeria still imported on the order of 2–3 Mt of wheat and rice through formal and informal channels). Many other countries import smaller quantities of wheat or rice to supplement local supplies. North Africa as a region dominates import volumes – for example, the four Maghreb countries (Egypt, Algeria, Morocco, Tunisia) together imported roughly 44 Mt of grain in 2024, mostly wheat. Sub-Saharan Africa’s imports are more fragmented, but West African nations collectively import very large quantities of rice (e.g. Nigeria, Côte d’Ivoire, Ghana, Senegal combined import over 6 Mt of rice) and wheat (Nigeria, Sudan, Kenya, etc).

Exporters: On the export side, only a few African countries are notable net exporters of grain. South Africa is the leading exporter – it often exports 2–3 Mt of maize per year (to Southern African neighbors, East Asia, and occasionally to the Middle East) and is among the top 10 maize exporters globally. Uganda and Tanzania sometimes export maize surplus to regional markets (e.g. to Kenya, Rwanda, DRC). Benin and Burkina Faso have re-exported imported rice into Nigeria (illicit trade responding to Nigeria’s import restrictions). Mali and Burkina Faso occasionally export small quantities of millet or sorghum within West Africa. Egypt has in some years exported rice when production exceeded domestic needs (though a ban since 2017 largely stopped this). Overall, intra-African grain trade is growing under regional trade agreements, but Africa remains a net importer by a large margin. The regional analysis highlights that food self-sufficiency varies significantly: countries like Zambia or Mali can be nearly self-sufficient in a good harvest year, while others like Somalia or Djibouti produce negligible grain and rely almost entirely on imports or food aid. This heterogeneity necessitates regional coordination – e.g., the new African Continental Free Trade Area (AfCFTA) aims to facilitate grain movement from surplus to deficit areas.

To summarize, Africa’s grain dynamics are shaped by a few heavyweights – Nigeria, Ethiopia, Egypt, and South Africa as production powerhouses, and North African and certain large SSA countries as consumption/import hubs. The interdependence is evident: for instance, Nigeria and Ethiopia mostly feed themselves but import some wheat; Egypt produces a lot yet must import vast wheat volumes to feed its population; South Africa’s exports help supply deficit neighbors. Strengthening regional trade links and boosting production in more countries will be key to balancing these regional disparities.

Trade Analysis (Imports, Exports, and Key Trade Partners)

Africa’s grain trade profile is characterized by high import dependency and relatively low export volumes, with a few key commodities and partners dominating the flow.

Import Volume and Value: In 2024, Africa imported approximately 71 million metric tons of cereals (total of all grains). This marked a rebound (+15% year-over-year) after a slight dip in imports during 2021–2023. The import volume has grown at an average of +2.3% per year since 2013 as consumption outpaced production. The cost of these imports has been rising even faster due to higher global grain prices – the import bill in 2024 surged to $27.3 billion. Over the last decade, the value of cereal imports into Africa increased ~5.3% annually. By 2024, imports were about 68% higher in value than in 2018, reflecting both greater volumes and price inflation. This growing expenditure on imported staples is a major concern for policymakers, as it impacts foreign exchange reserves and trade balances. African leaders have noted that if current trends continue, the continent’s food import bill (for major foods) could double in the next 10 years, underscoring urgency to boost local production.

Composition of Imports: The import mix is heavily skewed toward wheat and rice:

- Wheat is the single largest imported grain, making up about 67% of Africa’s cereal import volume. In 2024, wheat imports were roughly 47 Mt. This reflects widespread demand for bread and wheat flour products across the continent and limited domestic production. Wheat imports have also been the fastest-growing (CAGR +5.1% from 2013–2024), indicating increasing reliance.

- Maize accounts for around 27% of cereal imports, at ~19 Mt in 2024. Interestingly, maize import volumes have shown a downward trend in recent years (–2.2% per year over 2013–2024). This suggests that African maize production growth (especially in countries like Zambia, Ethiopia, Malawi) has reduced the need for imports, and at times Africa collectively produces most of the maize it consumes. The share of maize in imports fell by ~17 percentage points over the last decade while wheat’s share rose equivalently.

- Rice is a major imported staple as well. While the index data above didn’t explicitly list rice under “cereals” (possibly treating it separately), external sources show that Africa’s rice imports (milled) were on the order of 20–25 Mt in 2024 (with Sub-Saharan Africa at ~28 Mt including stock buildup). Rice likely constitutes a large portion of the remaining cereal import pie beyond wheat and maize. In value terms, rice imports cost Africa many billions of dollars annually (e.g., Nigeria alone used to spend $1–2 billion on rice imports before recent restrictions).

- Barley made up about 5% of imports (3.7 Mt) in 2024, mainly going to North Africa for beer brewing and animal feed.

- Other grains like sorghum and millet are imported only in very small quantities (occasionally by food aid agencies or niche industries). There is some import of malting barley, brewing sorghum, and rice bran for processing, but collectively these are marginal.

In summary, wheat and rice are by far the most critical import commodities for Africa’s food security. Dependence on external markets for these staples leaves countries exposed to supply shocks and price volatility.

Key Import Partners: Africa sources its grain imports from a relatively small number of global suppliers:

- Wheat imports come primarily from the Black Sea region (Russia, Ukraine), the European Union (France, Germany, Lithuania), North America (Canada, USA), and Argentina/Australia depending on price and quality. In recent years, Russia emerged as the top wheat supplier to Africa. For example, North African countries like Egypt and Sudan import substantial wheat from Russia and Ukraine – prior to 2022, about 37% of Sub-Saharan Africa’s cereal imports were from Russia/Ukraine. The Ukraine war initially disrupted this trade, but agreements and shifts to other suppliers prevented a collapse. France remains a key wheat source for francophone Africa (e.g., Algeria’s tenders often source French wheat). Canada and USA provide high-protein wheat for blending. Wheat trade is often structured through government or large grain traders; e.g., Egypt’s GASC (General Authority for Supply Commodities) tenders for millions of tons of wheat each year on global markets.

- Rice imports come overwhelmingly from Asia. India is the largest rice exporter to Africa (especially of parboiled rice favored in West Africa). Thailand and Vietnam are also major suppliers, particularly of white rice for East and Southern Africa. Pakistan exports long-grain white rice to Eastern Africa. In West Africa, about 70% of imported rice traditionally came from Thailand and Vietnam, but India has increased its share in recent years. Notably, in late 2022 and 2023, India’s restrictions on broken and non-basmati rice exports forced African importers to temporarily shift to Thai and Pakistani rice. China has also started exporting some rice to African markets. Sub-Saharan Africa now buys more than 40% of globally traded rice, making it a key market for Asian exporters.

- Maize imports are sourced from countries like Brazil, Argentina, Ukraine, and the US. For example, Egypt (one of Africa’s top maize importers for feed) buys maize from Ukraine and Brazil. Kenya and Zimbabwe often import white maize from neighboring countries (Uganda, Tanzania, Zambia) or Mexico/Ukraine in drought years. South Africa’s feed industry sometimes imports yellow maize from Argentina if regional prices are high.

- Barley imports into North Africa come from the EU, Russia, and Ukraine mainly. Algeria, Tunisia, and Morocco import feed barley for livestock when local production falls short.

- For other grains: Canada and Australia have supplied small quantities of malting barley or oats; Argentina has exported sorghum to Spain via African ports (transshipments), etc., but those are minor.

It’s worth noting that intra-African trade is growing under regional blocs. For instance, East African countries trade maize and rice among themselves (Uganda->Kenya maize, Tanzania->Kenya rice, etc.), West African countries trade coarse grains across borders (e.g., Mali exports millet to neighbors in the Sahel in good years). The AfCFTA is expected to further reduce barriers for such trade. Still, the bulk of net imports are supplied from outside Africa.

Exports and Intra-African Trade: As mentioned, Africa’s grain exports are limited:

- Maize: South Africa leads with typically 1–3 Mt exported annually, often to Zimbabwe, Mozambique, Botswana and occasionally to Japan, South Korea, Taiwan (South Africa exported to Asia during global shortages in 2021). Other exporters include Uganda (to regional markets like South Sudan, Kenya) and Tanzania (to Kenya, Rwanda in deficit years). In 2022, strong harvests saw Uganda and Tanzania export more maize within East Africa.

- Rice: Mali and Uganda have very small cross-border rice exports within Africa. Egypt used to export rice (over 1 Mt/year in the mid-2000s) but now has export bans to conserve water.

- Sorghum: Sudan occasionally exports sorghum (e.g., to World Food Programme for regional food aid). For instance, Sudan sold sorghum to WFP operations in Yemen and the Horn of Africa in past decades. Volumes are modest (100-200 kt in good years).

- Wheat: Virtually no exports, since no African country produces surplus wheat. (Some re-exports happen: e.g., South Africa might re-export small volumes of imported wheat flour to neighbors.)

- Barley: No significant exports.

- Processed products: There is some export of value-added products like pasta or flour within Africa (e.g., Morocco exports pasta to West Africa; South African millers export maize meal to regional markets; Nigeria has exported pasta/noodles to neighbors). But again, these volumes are small relative to imports.

Trade Balance: Africa runs a large structural trade deficit in cereals. As of 2021, Africa’s net imports of major food products (including grains) was around $39 billion per year. The grain trade deficit contributes significantly to that. Figure 4A in the AGRA report shows that Africa’s agricultural imports (in USD) have consistently exceeded exports over the last decade, with a net trade deficit reaching about $35–40 billion by 2020. While African countries do export high-value cash crops (cocoa, coffee, tea) and some commodities (fruits, nuts), those earnings do not offset the spending on grain, oil, and sugar imports.

This dependency has prompted calls for a “food import substitution” strategy. Reducing imports of basics like wheat and rice through local production is a policy priority in many countries. However, achieving that is challenging in the short term. In the meantime, managing trade – e.g., through better storage to even out supply, regional agreements to avoid export bans, and maintaining strategic grain reserves – is critical. The volatility of world markets is a constant risk: for example, when India banned rice exports in mid-2023, prices spiked, affecting many African consumers; similarly, droughts or export restrictions in supplier countries can quickly lead to shortages.

In summary, Africa’s grain trade is characterized by heavy reliance on imports, predominantly of wheat and rice from Eurasia, with only one significant export (maize from South Africa). The trade networks are relatively well-established – global grain traders (like Cargill, Louis Dreyfus, Olam) and state buying agencies handle large flows into Africa. One silver lining is that some African countries with comparative advantages in certain grains (maize in Southern Africa, rice in West Africa’s lowlands) could expand production and increase intra-African trade, thereby reducing the need for overseas imports. The Continental Free Trade Area could facilitate such shifts. For now though, Africa remains the world’s fastest-growing grain import market, which is both an opportunity for global exporters and a vulnerability for African economies.

Production and Consumption Trends

Historical Production Trends: Africa’s grain production has been on a generally upward trend in absolute terms, but growth has been gradual and inconsistent. Total cereal output in Africa increased from roughly 180 Mt in the early 2010s to about 218 Mt by 2023. The year 2023 saw a peak production around 218 Mt, before a slight drop in 2024 due to weather setbacks. Over the 2013–2024 period, production volume grew at only a mild rate (roughly ~1–2% per year on average), insufficient to match population growth. The positive trend in output was largely driven by expansion of harvested area in some countries and modest yield improvements in others. However, cereal yields in Africa remain very low – averaging only ~1.7 tons per hectare in 2024. This is essentially flat compared to a decade ago (1.7 t/ha in 2021 and no significant gains through 2024). By contrast, the global average cereal yield is about 4.15 t/ha – more than 2.5 times Africa’s average (1.63 t/ha). Such low productivity means Africa has to cultivate vast areas (often through area expansion) to increase output, which is not sustainable indefinitely.

The reasons for slow production growth are well documented: limited use of quality inputs (fertilizers, improved seeds), low mechanization, predominant rain-fed agriculture (exposing crops to drought risk), and soil fertility issues. For example, fertilizer application in Africa is about 17 kg/ha on average – a fraction of the global average – contributing to yield gaps. There have been some bright spots: certain countries achieved notable production gains. From 2013 to 2024, among major producers, Ghana showed the fastest production growth (CAGR +6.4%) due to policies like Planting for Food and Jobs (boosting maize output). Ethiopia nearly doubled wheat production in the late 2010s through aggressive extension programs. Malawi and Zambia had years of bumper maize crops following subsidy programs. Yet, these successes are not uniform across the continent.

Historical Consumption Trends: On the consumption side, the trend has been steadily upward with few interruptions. Africa’s cereal consumption (for food, feed, seed, and industrial use combined) rose from ~230 Mt in 2013 to 283 Mt in 2024, as noted earlier. This 53 Mt increase represents the rising needs of an expanding and urbanizing population. Notably, food use (human consumption) constitutes the bulk of cereal utilization in Africa – most of the maize, sorghum, millet, and rice go directly into diets. However, feed use is growing as well in countries with developing livestock sectors. For instance, the continent’s feed production was about 44.2 Mt in 2021 (for poultry, fish, cattle, etc.), a 2.4% increase from the previous year, reflecting more maize and soybean being diverted to animal feed. This is especially true in countries like South Africa, Egypt, and Morocco, where large-scale poultry and dairy farms drive maize and barley demand.

Year-to-year consumption has generally risen, except in rare cases of economic downturn or spiking prices which can temporarily suppress demand. The trend pattern remained relatively stable, with minor fluctuations – e.g., consumption growth slowed in 2020 due to COVID-related recessions but then picked up by 2024 (rising 3.6% from 2023). Importantly, consumption growth (1.9%/yr) has outpaced production growth (~1.0–1.5%/yr), leading to an increasing import requirement over time.

Changing Dietary Patterns: One of the most significant consumption trends is the changing composition of diets:

- Urbanization and Income Growth are shifting preferences toward wheat and rice and away from traditional coarse grains in many areas. Urban consumers value convenience and variety: bread, noodles, pasta, and rice are often easier to prepare or are preferred status foods compared to millet or cassava. As a result, per capita wheat and rice consumption has risen notably in Africa’s cities. For example, per capita wheat consumption in sub-Saharan Africa grew ~25% in the last two decades, and rice consumption grew ~40%. In contrast, per capita maize consumption has been flat or declining in some urban areas (though it remains high in rural diets).

- Continued reliance on traditional staples persists in rural areas. Many farming households consume what they grow – so in the Sahel, millet/sorghum remain principal foods, and in East/Southern Africa, maize remains king. There is also a cultural element: for instance, teff in Ethiopia or fufu (made from maize, plantain, cassava mixes) in West Africa remain important.

- Rise of processed and value-added grain foods: As economies develop, more grains are consumed in processed forms (breakfast cereals, fortified flours, instant noodles, beer, etc.). This creates downstream industries but also can increase grain demand (e.g., malting barley for beer).

- Animal feed demand: While still a smaller slice of total usage than in industrialized regions, feed demand for grains in Africa is rising with the growth of poultry farming and aquaculture. Maize is the main feed grain (along with some sorghum and millet in dry areas, and imported feed wheat or broken rice occasionally). Countries like Egypt channel a significant portion of maize imports into poultry feed. Feed demand ties grain markets to meat consumption trends; as Africans consume more chicken and farmed fish with rising incomes, this indirectly boosts grain consumption.

Geographic Shifts: Consumption is rising fastest in West and Central Africa, where population growth is highest, and where rice/wheat are increasingly important. Eastern Africa has seen strong growth too (Ethiopia, Kenya). Southern Africa’s consumption growth is a bit slower, constrained by smaller population growth and already high per-capita maize consumption in countries like Zambia or Malawi.

Self-Sufficiency Trends: An important indicator is the cereal self-sufficiency ratio (SSR) – the share of consumption met by domestic production. Africa’s overall SSR for cereals has been declining. In 2000, Africa produced roughly 80% of what it consumed; today that figure is closer to 60–70%, depending on the year. This decline means imports filled the gap. For certain staples: maize SSR is relatively high (Africa generally produces ~90%+ of its maize needs, with occasional surpluses), whereas wheat SSR is very low (~30%), and rice SSR around ~60%. Sorghum/millet SSR is nearly 100% (since little is imported). Thus, trends show Africa becoming more self-sufficient in some indigenous crops (maize, due to yields and area expansion) but less so in introduced staples (wheat, rice) that have grown in preference.

Climate and Shocks: Weather shocks have a large impact on year-to-year production (and therefore on imports and consumption smoothing). For example, droughts in Southern Africa (as in 2016 and 2019) sharply cut maize harvests, leading to higher imports and even food insecurity in affected countries. Similarly, drought in Morocco or Algeria drastically reduces wheat output, spiking their import needs. Climate change is expected to increase the frequency of such shocks. Africa’s overall cereal output variability is among the highest globally, which complicates planning. On top of weather, pests and diseases have emerged – the invasion of the Fall Armyworm across Africa since 2016 caused up to 33–50% maize yield losses in affected areas and an estimated $9.4 billion in annual damage if uncontrolled. Locust swarms in East Africa in 2020 also threatened crops. These episodic events affect trends by periodically knocking back production gains.

Post-Harvest Losses: Another trend in focus is reducing losses. Currently, a significant portion of grain produced never reaches consumers due to post-harvest losses (estimates range from 10% to 20% lost to inadequate storage, pests, spillage, etc.). Efforts to improve storage (metal silos, hermetic bags) and drying could effectively increase available supply without raising production. This is a priority in many countries.

In summary, the trends in African grain production and consumption show a widening gap: consumption has maintained a strong upward trajectory driven by demographics and diet change, whereas production is increasing but not fast enough. Consequently, imports and food aid have effectively become Africa’s “second harvest,” making up the difference. Without major interventions, this pattern will likely continue. However, there is significant scope to alter these trends – even modest improvements in yield growth (from ~1% to 2–3% annually) could dramatically change the outlook by 2035, potentially allowing Africa to meet a much larger share of its grain demand internally. The later sections on drivers, innovations, and investments will discuss how current trends could be bent toward a more self-reliant trajectory.

Market Drivers and Challenges

The African grain industry’s future is shaped by a complex mix of drivers (“tailwinds”) that support growth and challenges (“headwinds”) that constrain it. Below we outline the key factors on both sides:

Key Market Drivers:

- Rapid Population Growth and Urbanization: Africa’s population is the fastest-growing in the world, increasing ~3% per year in many countries. This means millions of new mouths to feed each year, directly boosting demand for staple grains. Additionally, Africa is urbanizing at ~3.5% per year – as people move to cities, their diets shift toward purchased and often grain-based foods (e.g., bread, pasta, rice dishes). Urban dwellers also eat more animal products, indirectly increasing grain demand for feed. Simply put, demographic momentum ensures a growing market for grains for the foreseeable future.

- Economic Growth and Rising Incomes: Pre-pandemic, many African economies saw sustained GDP growth, which is gradually resuming. As household incomes rise (even modestly), food consumption typically increases in quantity and quality. Dietary diversification occurs, but in low-income segments it often means consuming more of affordable staples and switching to preferred grains (for example, from cassava to rice, or from sorghum to wheat bread). Middle-class growth also expands markets for higher-value grain products (breakfast cereals, beer, etc.). Overall, income growth tends to raise per capita grain consumption until higher income levels are reached. Africa also has a large youth population, whose changing preferences (more wheat and rice, convenience foods) are influencing grain demand.

- Government Policies Aimed at Food Security: Many African governments have prioritized increasing grain production and reducing food imports. Initiatives under the Comprehensive Africa Agriculture Development Programme (CAADP) and national schemes provide support to grain farmers. Examples include:

- Input subsidy programs (for fertilizer, seeds) in countries like Malawi, Zambia, Ghana, Nigeria, which have boosted maize output.

- Mechanization and irrigation investments (e.g., Nigeria’s purchase of tractors, expansion of irrigation in Sudan and Ethiopia’s lowlands for wheat).

- Price support or guaranteed minimum prices for cereals (e.g., Burkina Faso’s grain marketing board).

- Strategic grain reserves that encourage production by ensuring markets for surplus. These interventions, though varied in success, demonstrate strong political will to grow the grain sector and can stimulate production when well-implemented. The African Union’s Malabo Declaration (2014) set a target to end hunger by 2025 and double agricultural productivity – while that target is off-track, it has galvanized efforts. More recently, the AU in 2023 adopted a ten-year strategy to increase Africa’s agro-food output by 45% by 2035, indicating continued commitment to driving grain sector growth.

- Untapped Agricultural Potential: Africa possesses abundant land and water resources that could be leveraged to expand grain production. It is often cited that Africa holds 65% of the world’s uncultivated arable land. While not all this land is readily available or conflict-free, there are regions (e.g., South Sudan, D.R. Congo’s savannas, Angola, Mozambique’s corridors) with scope for responsible agricultural expansion. Similarly, the potential for irrigation is huge – only ~4% of cropland in sub-Saharan Africa is irrigated, versus 20% globally, so there is room to develop water for dry-season or drought-resilient grain farming. This latent potential acts as a driver in the sense that investors and governments see opportunity for big gains through modernization and expansion of agriculture. If tapped sustainably (with proper investment in infrastructure and land management), Africa could dramatically raise its grain output – studies suggest Africa could produce 2–3 times more cereals than it currently does if yield gaps and resource use are addressed.

- Growing Regional Trade and Integration: The push for intra-African trade (via AfCFTA and regional blocs) is a driver for the grain industry. Improved regional trade means farmers in surplus zones have larger markets, incentivizing production. For instance, maize farmers in Zambia can target demand in food-deficit Zimbabwe or DRC; East African grain traders can ship maize from Uganda to Kenya, or rice from Tanzania to Uganda, more easily as tariffs and trade barriers fall. Integration also encourages investment in cross-border grain value chains (storage hubs, transport corridors, commodity exchanges). Over time, this can stabilize markets and stimulate farmers to produce more, knowing they can sell regionally. Greater market access = larger effective demand = incentive to increase supply.

- Private Sector and Foreign Investment: There is rising interest from agribusiness firms and foreign investors in African agriculture. Large commodity traders (like Olam, ETG, Cargill) are investing in grain handling and processing facilities. Investors from the Middle East, India, and China have at times invested in African farmland or in contract farming to secure grain supplies. While so-called “land grabs” have been controversial, responsible investments bringing capital, technology, and market linkages can drive production. Additionally, domestic entrepreneurs are setting up rice mills, feed mills, and flour mills across Africa, creating a pull for raw grain from farmers. The growth of Nigeria’s and Ghana’s rice milling capacity in recent years, for example, has driven more rice cultivation. Access to financing for farmers (through microfinance or contract farming schemes) is slowly improving, enabling them to adopt yield-enhancing technologies. All these private-sector trends help push grain output and efficiency upward.

- Technological Advancements: (This is elaborated in its own section later, but in brief as a driver:) New seed varieties (drought-tolerant maize, short-cycle rice, biofortified millet), better agronomic practices (such as microdosing fertilizer or “Smart” climate-adapted farming), and digital tools (market information systems, mobile finance, etc.) are beginning to bear fruit in Africa. For instance, improved maize hybrids and the spread of fall armyworm-resistant maize lines are expected to mitigate pest losses. Innovations like digital weather advisories and insurance encourage farmers to invest in planting. Over time, these tech-driven improvements contribute to yield growth, making them a driver of future grain supply increases.

Major Challenges:

- Low Farm Productivity: Arguably the most fundamental challenge is Africa’s low crop yields. As noted, cereal yields average ~1.7 t/ha in Africa, versus ~4 t/ha globally, and >6 t/ha in North America. This yield gap stems from multiple factors:The net effect is that even though African farmers work hard, the output per hectare and per farmer is low, keeping production volumes insufficient. Raising productivity is the key to addressing many other issues (like imports and rural poverty).

- Limited Irrigation: Only ~4% of cropland in sub-Saharan Africa is irrigated, meaning 96% is rain-fed and highly vulnerable to droughts and erratic rainfall. Many regions have only one short growing season. Insufficient water control drastically limits yields for rice and wheat in particular.

- Low Fertilizer and Input Use: Fertilizer use is the lowest of any region; many smallholders use none or well below recommended rates (the Abuja Declaration target of 50 kg/ha by 2015 was missed by a wide margin). Access to quality seeds is also a problem – adoption of improved varieties is far from universal. Without soil nutrients and good seeds, yield potential remains low.

- Minimal Mechanization: The majority of African grain is produced by smallholders with hand tools or animal traction. Tractor penetration is very low (perhaps 2 tractors per 1,000 ha in Africa vs 10+ in Asia). This limits the area a household can cultivate and can delay planting/harvesting, impacting yields and losses.

- Land Degradation: Soil fertility depletion, erosion, and land degradation afflict large areas. Africa loses significant cereal production each year due to degraded soils (for example, an estimated 280 million tons of cereal yield is lost annually from land degradation according to some reports). Restoring soils and using climate-smart practices is a challenge that must be overcome to improve productivity.

- Farm Size and Labor Constraints: Many farms are very small (<2 ha) and fragmented, making it hard to achieve economies of scale or justify mechanization. Labor productivity is low; farming is often largely subsistence-oriented.

- Climate Change and Weather Variability: Africa’s grain production is extremely vulnerable to weather shocks. Droughts, erratic rainfall, and extreme heat are already common and expected to intensify with climate change. Many grain-growing regions (e.g., the Sahel, Southern Africa, Horn of Africa) have seen increased frequency of drought in recent decades. When rains fail, maize and other crops wither – as seen in the 2011 Horn of Africa famine and frequent Sahel droughts. Climate change poses a severe threat by potentially reducing yields 5–30% in many areas by 2050 if no adaptation occurs. It also brings unpredictability: planting rains might be delayed or end early, harming crop cycles. Floods can also destroy crops (Mozambique had devastating floods affecting maize fields in 2019). The challenge is magnified by the lack of irrigation buffering and limited resilience measures. Without major adaptation (drought-tolerant varieties, expanded irrigation, climate-smart farming), climate change could negate gains and further widen the production-consumption gap. In addition, climate variability complicates storage and marketing – a bumper year followed by a drought year leads to price swings and instability.

- Pests, Diseases, and Post-Harvest Losses: Agriculture in Africa faces persistent biological challenges:Combating these pests and losses requires better extension services, access to crop protection products, training in storage, and investments in rural infrastructure like silos and drying equipment. While progress is being made (e.g., adoption of hermetic storage bags is increasing, and regional cooperation on locust control exists), it remains a big challenge to protect the grain that is grown.

- Insect pests like the Fall Armyworm (Spodoptera frugiperda) since 2016 have caused maize losses up to 20–50% in affected regions, with economic damage estimated around $9.4 billion annually. Other pests include stem borers, locusts (the 2020 desert locust upsurge threatened East African crops), grain-eating birds (quelea devastate small grains), etc.

- Plant diseases (maize lethal necrosis, wheat rusts, rice blast) also threaten yields. A wheat stem rust (Ug99) that emerged in East Africa requires constant vigilance and breeding of resistant varieties.

- Post-harvest pests (storage weevils, rodents, fungi) cause significant losses during storage. For example, without proper drying and storage, maize can develop aflatoxin from fungal infection, making it unfit for consumption and causing economic loss.

- Post-harvest losses in general are a challenge – lack of drying facilities, inadequate storage (most smallholders store grain in bags that are not pest-proof), and poor rural transport lead to spoilage and spillage. These losses can claim 10–15% or more of the harvest in many areas, effectively reducing available food and farm incomes.

- Insufficient Infrastructure (Storage, Transport, Processing): African farmers and traders face high costs and inefficiencies due to infrastructure gaps:These infrastructural challenges increase wastage and costs, making African grain less competitive and constraining market growth. Addressing these requires heavy investment and coordinated policy (e.g., warehouse receipt systems, farm-to-market road projects, etc.).

- Transport: Poor rural roads and long distances raise the cost of moving grain from farm to market or port. In some countries, up to 30% of the value of grain is eaten by transport costs. This makes local grain less competitive and can discourage farmers from producing surplus (if they can’t get it to market cheaply). Inland countries (e.g., Chad, South Sudan) face immense challenges accessing global markets.

- Storage and Market Facilities: There is a shortage of modern grain storage facilities (silos, warehouses). Many countries lack sufficient public grain reserves or warehouse systems. This leads to seasonal gluts and price collapses post-harvest in some cases (hurting farmers), followed by scarcity and high prices pre-harvest (hurting consumers). The inability to effectively store surplus from good years to use in bad years is a structural weakness. For example, in East Africa, limited regional storage contributes to recurrent shortages during droughts.

- Processing and Value Addition: While there are milling facilities in most countries, some regions lack adequate local mills, meaning farmers must sell raw grain at lower value and countries import processed products at higher cost. This is changing with more investments in mills, but the processing sector is uneven. In some cases, local production is dis-incentivized by cheaper imports of flour or meal if tariffs are low.

- Irrigation and Energy Infrastructure: As mentioned, irrigation systems are underdeveloped. Also, energy access is low in rural areas, affecting agro-processing and storage (e.g., lack of electricity for cold storage or milling operations).

- Policy and Market Instability: Policy inconsistency can be a major challenge for the grain sector:In summary, unpredictable policy and instability raise the risk for producers and traders. A more stable, transparent policy environment is needed to build confidence in the market.

- Some governments impose export bans or trade restrictions during times of shortage (e.g., Malawi or Tanzania have at times banned maize exports to protect local supply). While understandable, these measures can discourage farmers from producing surplus (knowing they might not export it in a glut) and can undermine regional trade.

- On the flip side, sudden import tariff changes or import bans (like Nigeria’s border closure to rice in 2019) can disrupt markets. If not well signaled, policies like price controls, ad-hoc subsidies, or government purchasing can create uncertainty for producers and traders.

- Limited access to credit/finance is another systemic issue – farmers and small agribusinesses often cannot get affordable loans to invest in yield-boosting technologies or storage, which is partly due to weak rural finance policy and risk perceptions.

- Political instability and conflict in certain regions also severely affect grain markets. For instance, ongoing conflicts in the Sahel (Mali, Burkina Faso) disrupt farming and trade routes; civil war in South Sudan and Somalia has led to chronic food crises; the insurgency in northern Nigeria hampers agriculture in a fertile region; the war in Sudan in 2023 has imperiled that country’s upcoming harvests of sorghum and wheat.

- Governance issues and corruption can affect the grain sector – mismanagement of strategic grain reserves, delayed payments to farmers by government agencies, etc., can all discourage production.

- Import Dependency and Global Price Volatility: Africa’s heavy reliance on imports of wheat and rice is itself a challenge, as it exposes the continent to global market fluctuations. Price spikes – like the 2008 global food crisis or 2022’s surge in wheat prices after Russia’s invasion of Ukraine – can hit African consumers hard, leading to food inflation and even unrest (the 2008 food riots in parts of Africa were partly over bread prices). When the global supply tightens, African countries (often being price-takers with limited bargaining power) suffer. The currency depreciation in some countries also makes imports pricier in local terms. All of this volatility makes planning difficult. Governments often respond with emergency measures (like reducing import tariffs or consumer subsidies) which can strain budgets. Until Africa can produce more of its own grain, it will remain vulnerable to such external shocks – a structural challenge that underpins the urgency to invest in local production capacity.

In conclusion, the drivers and challenges in Africa’s grain industry are two sides of the same coin. Robust demand growth and untapped potential provide huge opportunity, but fulfilling that potential requires overcoming significant hurdles in productivity, infrastructure, and resilience. The interplay of these factors will determine whether Africa can turn its grain sector into a success story of meeting its own needs (and even exporting), or whether it will continue along the path of greater import dependence. The next sections on policy, competition, and technology will delve into how the continent is attempting to address these challenges and leverage the drivers.

Policy and Regulatory Landscape

Agricultural and trade policies play a critical role in shaping Africa’s grain industry. Over the past two decades, African governments and regional bodies have launched numerous policies, initiatives, and regulatory frameworks aimed at boosting grain production, ensuring food security, and managing trade. Below, we outline the key elements of this policy landscape:

- Comprehensive Africa Agriculture Development Programme (CAADP): At the continental level, CAADP (established by the African Union in 2003) has been the overarching framework guiding agricultural policy. Under CAADP, African leaders committed to allocate at least 10% of national budgets to agriculture and achieve 6% annual ag GDP growth. While many countries fell short of the 10% target, CAADP has spurred increased investment and policy attention to agriculture, including grains. It also emphasized regional collaboration and funding for research (e.g., for improved grain varieties). The Malabo Declaration (2014) was a recommitment to CAADP goals, with specific targets like ending hunger by 2025, doubling productivity, and halving post-harvest losses. As of the latest Biennial Review, Africa is not on track to meet the hunger eradication goal by 2025, indicating more work needed. However, CAADP has institutionalized the practice of evidence-based ag policy planning in many countries (through National Agriculture Investment Plans), often prioritizing grains as key staples.

- National Food Security Programs: Virtually every African country has some policy initiative focused on staple grain self-sufficiency or food security:

- For example, Nigeria has periodically banned or placed tariffs on rice and maize imports to protect local farmers, and launched programs like the Anchor Borrowers’ Programme (providing credit to rice and wheat farmers) and Strategic Grain Reserve revamps. Nigeria’s goal is to become self-sufficient in rice and significantly raise local wheat production.

- Ethiopia runs an aggressive extension system and in recent years a Summer Wheat Irrigation initiative – the government coordinates large-scale irrigated wheat cultivation in lowland areas to eliminate wheat imports. Subsidized credit and mechanization support are also provided.

- Egypt heavily manages its grain sector: it has a longstanding bread subsidy program where the government buys millions of tons of wheat (domestically and imported) to supply bakeries at controlled prices. Egypt also sets local wheat procurement prices to incentivize farmers and has periodically banned rice exports to conserve water and ensure domestic rice availability.

- Kenya maintains a National Cereals and Produce Board (NCPB) that buys maize from farmers at administered prices and manages a grain reserve for stability. Kenya also waives import duties on maize during deficit periods and controls cross-border grain movement at times.

- South Africa, in contrast to many others, has a more liberalized grain market since the 1990s (no parastatal grain board now), but the government provides general support (research, extension) and monitors food prices closely.

- Morocco has a program called “Maroc Vert” (Green Morocco Plan) and its successor “Generation Green” which include pillars for cereal yield improvement and crop insurance for drought years. Morocco adjusts tariffs on wheat (often imposing high tariffs during domestic harvest to favor local wheat, then lowering them later to stabilize consumer prices).

- Many West African countries work under ECOWAS policies to maintain moderate common external tariffs on grains (for instance, ECOWAS CET puts 10% tariff on rice and 5% on wheat, with some flexibility per country). They also have regional reserves (ECOWAS has a Regional Food Security Reserve) to aid in crises.

- Trade Policies and Regional Agreements: Africa’s regional economic communities (RECs) – ECOWAS, EAC, SADC, COMESA, etc. – have frameworks affecting grain trade.

- For instance, ECOWAS has ratified the ECOWAS Agricultural Policy (ECOWAP) which mirrors CAADP goals and promotes intra-regional trade of food products. It also set up mechanisms to coordinate food security stocks.

- EAC (East African Community) has had instances of joint approaches, like allowing duty-free imports of maize during droughts affecting member states, and discussing elimination of non-tariff barriers on grain trade between members.

- SADC has a regional early warning system for food security and generally low tariffs on intra-SADC grain trade, but countries like Zambia or Malawi have unilaterally imposed export bans at times, causing continuing from Policy and Regulatory Landscape:

… hindered regional grain market integration (highlighting the need for AfCFTA implementation).

- African Continental Free Trade Area (AfCFTA): Launched in 2021, AfCFTA is a game-changing pan-African trade pact aiming to eliminate tariffs on up to 90% of goods (including many agricultural products) and harmonize trading standards. Though still in early stages, AfCFTA promises to lower barriers for grain trade across African border. Over time, it should reduce the reliance on overseas imports by enabling surplus grain from one African region to more easily reach deficit regions. It also encourages investment in cross-border infrastructure and standardizes regulations (for example, sanitary and phytosanitary standards for grain quality). The successful implementation of AfCFTA could boost intra-African grain trade significantly from its current low base (estimated <20% of Africa’s grain trade is intra-continental). In essence, AfCFTA’s regulatory framework is set to create a single African market for grains, which can improve efficiency and prices.

- Biosafety and Quality Regulations: African governments are also grappling with regulations around new agricultural technologies and food safety:

- GMOs (Genetically Modified Organisms): Only a few African countries (South Africa, Sudan, Eswatini) currently allow commercial cultivation of GM grain crops (South Africa has widely adopted GM maize, leading to major yield gains). Most others have strict bans or are cautiously conducting trials (e.g., Kenya and Nigeria have trialed GM maize). This regulatory stance affects seed technology adoption – countries restricting GMOs forego potential yield improvements from pest-resistant or drought-tolerant GM varieties, but they prioritize biosafety and export market considerations. There is ongoing debate and gradual shifts: Nigeria approved Bt cowpea in 2019 (first GM food crop in Africa outside South Africa) and Kenya approved Bt cotton. The coming years may see more openness to GM maize or wheat if food security pressures mount, but for now regulatory hurdles remain a challenge for biotech companies.

- Fortification and Safety Standards: Many African countries have introduced mandatory fortification of staples (e.g., fortifying wheat flour or maize meal with vitamins/minerals) to combat malnutrition. This affects millers and grain importers (they must comply with standards). Additionally, regulations to curb aflatoxin contamination in maize and groundnuts are being strengthened – some countries set maximum allowable levels and promote better drying and storage to meet those standards. Harmonizing these quality standards regionally (through COMESA, EAC, etc.) is ongoing so that grain can move more freely without safety concerns.

- Strategic Grain Reserves and Price Controls: Some governments maintain legal frameworks for food price stabilization – authorizing strategic grain reserves to release stocks during shortages or capping prices of bread and maize meal to protect consumers. For example, Kenya’s NCPB operations, Zambia’s Food Reserve Agency buying at set floor prices, or Egypt’s bread subsidy and rationing system are part of regulatory approaches to manage affordability. While these can stabilize markets, they must be managed transparently to avoid distorting incentives for farmers.

In sum, Africa’s policy environment for grains is a mix of bold continental visions (CAADP/Malabo, AfCFTA) and pragmatic national measures aimed at self-sufficiency and price stability. The regulatory trends show a balancing act: encouraging production (through subsidies, research, land policies) and facilitating trade, while also protecting consumers (through subsidies, reserves, and import management). Going forward, stronger regional coordination – as exemplified by AfCFTA and AU’s commitment to boost output by 45% by 203 – will be crucial. The policy direction is clearly towards greater investment in agriculture and reduced trade barriers, but execution will determine results. For now, navigating the patchwork of national regulations remains part of doing business in Africa’s grain sector, and policy risks (like sudden export bans) are an ever-present concern that stakeholders must manage.

Competitive Landscape and Key Players

The competitive landscape of Africa’s grain industry is unique in that production is highly fragmented among millions of small farmers, while certain downstream activities (trading, milling) see more concentration and involvement of large players. Here’s an overview of the key players across the value chain:

- Smallholder Farmers: The backbone of grain production in Africa is the small-scale family farm. It is estimated that smallholders (farms under 2 hectares) produce up to 70–80% of Africa’s food output, including the majority of grains. There are around 33 million small farms in Africa, and they collectively dominate maize, millet, sorghum, and rice production. These farmers typically sell part of their harvest into local markets and retain the rest for family consumption. The production side of the grain industry is therefore very unconcentrated – no single farmer or farming company has more than a tiny share of output. Even in relatively commercialized grain sectors like South Africa’s maize belt, there are thousands of medium-sized farms rather than a handful of giant estates. This smallholder dominance has implications: improving grain supply means empowering vast numbers of these producers with inputs, finance, and market access.

- Large Commercial Farms: While smallholders prevail, there are notable larger farms and estates for certain crops/regions. For example, South Africa has large mechanized grain farms (some over 1,000 ha) producing maize and wheat at scale – companies like Senwes (a farmer-owned agribusiness) manage significant acreage and grain storage. In Sudan, large government-run schemes (Gezira) produce sorghum and wheat on tens of thousands of hectares (though performance has been mixed). Ethiopia has state or investor-run wheat and maize farms in lowland areas. Zambia and Zimbabwe have some commercial farmers (including a community of white Zimbabwean-origin farmers in Zambia) cultivating maize and wheat commercially. Also, foreign investment projects – e.g., by companies from India, China, and the Middle East – have acquired land for rice or wheat farming in countries like Nigeria, Senegal, and Ethiopia, though many projects haven’t reached full potential. Despite these, large farms still constitute a minor share of Africa’s grain output overall.

- Government Agencies and Parastatals: In many countries, government or quasi-governmental entities play key roles in grain markets:

- National strategic reserve agencies (e.g., Nigeria’s Strategic Grain Reserve Dept., Kenya’s NCPB, Zambia’s FRA, Malawi’s NFRA) purchase, store, and distribute grains. They can influence market prices and are major buyers in years of surplus. For instance, Zambia’s Food Reserve Agency has at times bought over 1 million tons of maize from farmers in a season.

- State importers: In some North African countries, state agencies handle grain import tenders. Egypt’s GASC (General Authority for Supply Commodities) is one of the world’s largest single wheat buyer, responsible for securing wheat for the subsidized bread program – its tenders effectively set benchmark prices. Similarly, Algeria’s OAIC (Office Algérien Interprofessionnel des Céréales) and Tunisia’s Office des Céréales import wheat and manage distribution to mills. These entities are powerful players in global markets and central to domestic grain supply.

- Marketing boards: While many marketing boards were liberalized in the 1980s-90s, a few remain or have been reintroduced in different forms (e.g., Ethiopia’s cereal trading enterprise, Ghana’s National Food Buffer Stock Company). They sometimes enjoy monopoly privileges or are significant traders domestically.

- Milling and Processing Companies: The milling industry (flour mills for wheat, feed mills for maize/soy, rice mills) is more consolidated than farming. Key players include:

- Local Champions: Flour Mills of Nigeria (FMN) is one of Africa’s largest flour milling groups, producing flour, pasta, and other grain product. Honeywell Flour Mills (recently merged with FMN) and Dangote Flour (Olam) are also big in Nigeri. In East Africa, Bakhresa Group (Tanzania) is a dominant miller present in milling and baking across multiple countries. In North Africa, companies like Les Grands Moulins (Morocco, Tunisia) are major wheat millers. SOMDIAA (a French company) operates flour and sugar mills in Francophone Africa. Tiger Brands (South Africa) through its Sasko division leads in maize and wheat milling in Southern Africa, alongside Premier FMCG and Pioneer Foods (now part of PepsiCo). These firms often have significant market shares in their countries for flour or maize meal.

- Multinational Agribusiness: Olam International (Singapore-based) is a notable player – originally focused on export commodities, Olam has expanded into African grain trading and milling (it operates wheat mills in Nigeria, Ghana, Senegal, Cameroon, etc. Seaboard Corporation (USA) has invested in flour mills in East and Southern Africa. Cargill is active in South Africa (maize trading and animal feed and has a grain trading presence in parts of Africa. ETG (Export Trading Group), based in East Africa, has become a significant regional grain aggregator and distributor. These companies bring global expertise and capital, and sometimes integrate the value chain from procurement to processing.

- Brewing and food companies: Large beverage and food companies indirectly shape grain demand – e.g., AB InBev/SABMiller and Heineken drive malting barley and sorghum demand through local beer production; Nestlé and Unilever purchase grains and starches for processed foods. These multinationals sometimes invest in local sourcing programs (contracting sorghum from farmers, etc.).

- Grain Traders and Commodity Exchanges: Trading of grains in Africa involves: